While Real Estate Investment Trusts (“REIT”) are US listed companies that own and operate real estate assets, in Brazil the equivalent real estate investment vehicle is known as Fundo de Investimento Imobiliário (“FII”).

FII were created in Brazil in 1993 and have experienced a huge expansion over the last years, boosted by regulation changes initiated in 2008. The Brazilian Securities and Exchange Commission (“CVM”) recently enacted the Resolution nº CVM 175, which was effective since October 2, 2023 (“RCVM 175”) and provides for the new regulatory framework governing investment funds in Brazil. In addition to its general part, which indistinctively applies to all investment fund categories, RCVM 175 now embodies a set of Normative Annexes, each of which provides for specific rules governing. The FII is treated in its Annex III.

As of the end of 2023, FII’s total assets under management (AuM) have reached to BRL 5,7 bi. It is a significant source of financing and an important channel of investments for Brazilian investors. Not only relevant in national terms, the Brazilian Capital Markets is progressively achieving more prominent roles on regional and global markets.

The FII is a close-ended fund that by pooling investors’ money to invest like a condominium in various segments of the real estate market such as offices, shopping centers, hotels, residence, logistic complex. This type of fund can also invest in securities.

Which assets can a FII hold?

FIIs can invest in:

• real estate rights on real estate property; and

• fixed income securities (CRI, LH, LCI, among others); and

• FIIs cannot invest in derivatives except for the purposes of asset protection.

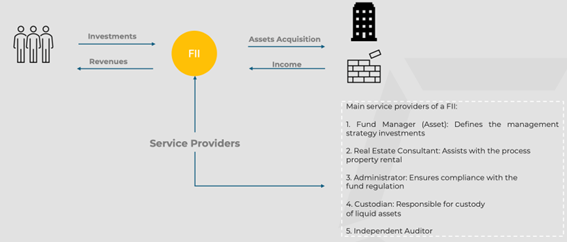

Summary Flowchart

Overview

The Fund Bylaws shall contain the main characteristics of the FII, including relevant information for investors about investment policies, risks involved, as well as quotaholders’ rights and duties. It shall contain at least the required elements listed below:

• Service providers as applicable;

• Target audience: A description of the target audience of the FII;

• Investment policy: Description of how the FII aims to achieve its investment goal, identifying the sectors in which it will operate, the nature of the investments that the FII will be allowed to make, i.e., the type of investments (real estate or financial assets) that will compose the portfolio;

• Investment concentration policy, when applicable: description of the investment diversification requirements and the asset selection and allocation policies;

• Amortization (when applicable) and payout policies: information about deadlines and payment terms;

• Share/Quotadescription: description of the different classes of quotas, whenever applicable, with the rights granted by each of them;

• Indication of any possible conflicts of interest: describe any possible conflicts of interest that may exist in the FII, pursuant to current legislation, and include them as risk factors in the Bylaws;

• Risk factors: indicate any and all facts related to the FII that may significantly affect prospective investors’ decision to purchase the FII’s quotas.

In addition to the regular Fund’s expenses, the FII can have the following expenses:

• commissions and fees paid on operations, including expenses related to the purchase, sale, acquisition or rental of properties;

• fees and expenses related to the activities provided for: (i) specialized consultancy, which aims to support and subsidize the activities of analysis, selection, monitoring and evaluation of real estate projects and other assets integrated or that may become part of the asset portfolio; and (ii) specialized company to manage the leases or properties, the exploration of surface rights, and monitor projects and the commercialization of the respective properties and consolidate financial data selected; and

• expenses necessary for the maintenance, conservation and repairs of properties forming part of the FII’s assets.

Best Practices for Conflict of Interest

Managing conflicts of interest (“COI”) in the fund management is crucial for ensuring integrity, and ethical decision-making. COI between FII and the administrator, manager or specialized consultant depend on prior, specific and informed approval by the Quotaholder Meeting. Examples of conflict of interest situations:

• the acquisition, leasing, rental by the FII of property owned by the administrator, manager, specialized consultant or people linked to them;

• the sale, acquisition or rental of FII property with the administrator, manager, specialized consultant or people linked to them as counterparty;

• the acquisition, by the FII, of property owned by developers from the administrator, manager or specialized consultant, once the debtor has defaulted;

• the hiring, by the FII, of people linked to the administrator or manager to provide specialized consultancy services; and

• the acquisition, by the FII, of securities issued by the administrator, manager, specialized consultant or persons linked to them.

General Advantages

• Negotiation stands out as a significant advantage in the context of FII shares compared to real estate transactions. Unlike the intricate and financially demanding nature of real estate dealings, FII shares are traded in a well-organized over-the-counter environment or on the Stock Exchange. This not only results in lower brokerage costs but also alleviates the burden of taxes associated with real estate transactions. The latter often entails extensive documentation and analysis, making it a more time-consuming process.

• The quality and management of real estate assets further contribute to the appeal of FII investments. FIIs boast professional management with dedicated teams overseeing properties that may not be readily accessible to the general public. This professionalism extends to the regulatory sphere, providing investors with a secure and transparent environment. In contrast, real estate transactions lack the same level of professional oversight, making FII investments a more streamlined and secure avenue for those seeking financial growth.

Tax Advantages

Foreign investors that (i) are not residents of a tax haven jurisdiction, and (ii) their investments are made in accordance with Central Bank regulations (Resolution nº 4373):

• 15% income tax withholding on FII distributions; and

• 15% capital gains tax on the sale or other transfer of FII quotas.

To foreign investors that are residents of a tax haven jurisdiction – same rate of Brazilian entities (20%).

In any case upon amortization or redemption of their quotas, and only to the extent that the amount amortized or redeemed exceeds the subscription price of the quotas.

Important: The FII must distribute at least 95% of the Fund’s earnings in the six-month period, calculated under the cash regime, in accordance with Law 8.668/93. Please note that if it proves unattainable on the designed structure, an alternative option is to consider a Real Estate FIP. In this scenario, the properties would be owned by the company in which the FIP has invested, limiting the ability to acquire additional real estate securities.