Prince William to Attend COP30 Climate Conference in Brazil: A Royal Commitment to Global Environmental Change

As the world anticipates the COP30 climate summit in Brazil next year, an important guest will be joining the ranks of global leaders and climate advocates: Prince William. Known for his passionate commitment to environmental causes, Prince William’s decision to attend the summit in Brazil signifies an important step in his advocacy for urgent climate action. His presence is expected to spotlight the importance of a united global response to environmental issues and underscore the British monarchy’s role in promoting sustainability.

At Finance Monthly, we take a closer look at what this attendance means in terms of international climate policy, the impact of Prince William’s commitment, and how his presence can influence public engagement and political commitment to tackling climate challenges.

The Significance of COP30 in Brazil

The 30th Conference of the Parties (COP30) to the United Nations Framework Convention on Climate Change (UNFCCC) is expected to be one of the most critical climate events in recent years. Hosted in Belém, Brazil—a region emblematic of both the world’s environmental richness and its vulnerability—COP30 will bring together countries, organizations, and activists to discuss climate policies, set actionable goals, and address the urgent threats facing the global ecosystem.

Brazil, home to the Amazon rainforest, is an especially relevant location for this summit, given the ongoing challenges around deforestation, biodiversity loss, and Indigenous land rights. The Amazon plays a critical role in regulating the Earth’s climate, and the fate of its ecosystem has far-reaching implications. Holding COP30 in Brazil places a special emphasis on the responsibility of all nations to protect these precious, shared resources.

Prince William’s Environmental Commitment

Prince William has long been an outspoken advocate for environmental protection, sustainability, and conservation. Through his foundation, the Royal Foundation of The Prince and Princess of Wales, William has launched several initiatives, including the ambitious Earthshot Prize. This prestigious award encourages individuals and organizations to propose innovative solutions to environmental challenges, with a specific focus on restoring and protecting the planet.

The Earthshot Prize, named in homage to President John F. Kennedy’s “Moonshot” speech, provides financial grants to fund promising solutions across categories like biodiversity conservation, climate repair, ocean revitalization, and waste elimination. By championing this initiative, Prince William has demonstrated that he is not only a figurehead but also an active participant in finding solutions to global challenges.

His involvement with COP30 is a continuation of this dedication, bringing attention to the need for international cooperation and innovative thinking in climate policy. Prince William’s high-profile attendance will likely amplify the urgency of climate issues, making it clear that protecting the planet is a cause that transcends borders and requires a truly global effort.

Why Prince William’s Attendance Matters

Prince William’s attendance at COP30 is expected to bring several key benefits:

- Raising Public Awareness: As a prominent member of the British royal family, Prince William’s influence is far-reaching. His participation in the summit will help raise public awareness around the world, mobilizing more individuals to take personal action against climate change and encourage their governments to implement sustainable policies.

- Political Influence: Prince William’s presence may serve to influence policymakers, motivating them to make meaningful commitments and collaborate on international climate goals. With his backing, climate pledges could be viewed with greater legitimacy and urgency, encouraging leaders to prioritize ambitious targets.

- Strengthening International Ties: The UK has historically been a strong advocate for climate action, and Prince William’s attendance can strengthen international relations on this front. His presence may foster greater cooperation with Brazil and other nations attending the summit, creating stronger bonds over shared environmental goals.

Prince William’s Broader Vision for Climate Action

Prince William has spoken publicly about his vision for a sustainable future, often highlighting the importance of global collaboration in addressing climate issues. He has been vocal about his desire to leave a livable planet for future generations, especially for his children. This deeply personal connection to environmental advocacy is central to his work, driving his commitment to initiatives like the Earthshot Prize.

At COP30, Prince William is likely to emphasize themes of unity, innovation, and resilience. His message will align with the larger goals of the summit, reinforcing the importance of coming together as a global community to face one of the most pressing challenges of our time.

What to Expect from Prince William at COP30

While Prince William’s specific role at COP30 has not yet been fully disclosed, he is expected to deliver a keynote address and participate in key discussions on climate policies. His speech is anticipated to focus on the importance of ambitious, actionable goals and the role of innovation in achieving a sustainable future.

Prince William may also highlight the achievements of the Earthshot Prize and discuss future opportunities for cross-border collaboration. His involvement at COP30 is likely to include meetings with world leaders, environmental advocates, and representatives from Indigenous communities, reinforcing the need for a collaborative approach to climate action.

The Prince’s agenda is also expected to include visits to local Brazilian communities and environmental projects, providing him with firsthand experience of the ecological challenges facing the region. This could allow him to gain deeper insights into Brazil’s unique climate struggles and strengthen his advocacy for more protective policies in regions critical to the global ecosystem.

The Role of the British Monarchy in Climate Advocacy

Prince William’s attendance at COP30 continues the British monarchy’s legacy of involvement in environmental conservation. His father, King Charles III, has been a vocal environmental advocate for decades, speaking out on issues like climate change, sustainable agriculture, and rainforest protection well before these topics became mainstream. King Charles’ environmental activism paved the way for Prince William to follow in his footsteps, with a renewed focus on practical solutions and global partnerships.

The British monarchy’s influence extends far beyond the UK, and by leveraging his position, Prince William can help build a bridge between leaders and communities who may otherwise struggle to connect over climate concerns. His attendance at COP30 will showcase the monarchy’s commitment to remaining relevant in a changing world, using its platform to support positive environmental change.

Prince William’s Influence on Future Generations

As a young, relatable member of the royal family, Prince William’s commitment to climate action resonates with younger generations. His approach is forward-thinking and optimistic, often focusing on practical solutions and encouraging innovation. By attending COP30, Prince William is signaling to young people worldwide that climate action is both necessary and achievable.

This involvement is likely to inspire a new generation of environmental leaders, urging them to take action on both individual and collective levels. His presence at the summit serves as a reminder that today’s decisions will shape the world for future generations, a message that aligns closely with the Earthshot Prize’s mission.

A New Chapter in Global Climate Advocacy

Prince William’s attendance at COP30 is more than a symbolic gesture—it’s a call to action. His involvement reaffirms the urgent need for global collaboration on climate policy and emphasizes the impact that prominent figures can have in mobilizing public support. With his focus on practical solutions, innovation, and sustainable development, Prince William is helping to lead a new chapter in climate advocacy that aims to bring tangible results.

By joining world leaders, environmental activists, and communities at COP30, Prince William demonstrates that climate change is a universal issue that demands everyone’s participation. His dedication to this cause will undoubtedly resonate during the summit and beyond, encouraging us all to work together toward a sustainable future.

Prince William’s commitment to attending COP30 represents a powerful statement about the importance of climate action and global cooperation. As he steps into this role, he will bring attention, inspiration, and influence to the international community’s efforts to combat climate change. At Finance Monthly, we celebrate his dedication and look forward to seeing how his participation can amplify the voices of climate advocates and inspire the world to take meaningful steps toward a healthier, more sustainable planet.

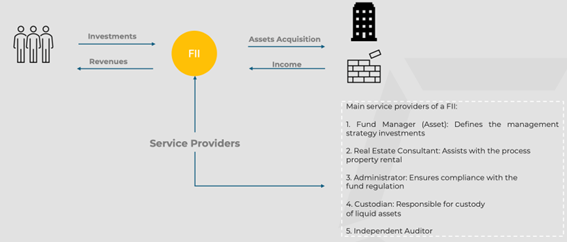

While Real Estate Investment Trusts (“REIT”) are US listed companies that own and operate real estate assets, in Brazil the equivalent real estate investment vehicle is known as Fundo de Investimento Imobiliário (“FII”).

FII were created in Brazil in 1993 and have experienced a huge expansion over the last years, boosted by regulation changes initiated in 2008. The Brazilian Securities and Exchange Commission (“CVM”) recently enacted the Resolution nº CVM 175, which was effective since October 2, 2023 (“RCVM 175”) and provides for the new regulatory framework governing investment funds in Brazil. In addition to its general part, which indistinctively applies to all investment fund categories, RCVM 175 now embodies a set of Normative Annexes, each of which provides for specific rules governing. The FII is treated in its Annex III.

As of the end of 2023, FII’s total assets under management (AuM) have reached to BRL 5,7 bi. It is a significant source of financing and an important channel of investments for Brazilian investors. Not only relevant in national terms, the Brazilian Capital Markets is progressively achieving more prominent roles on regional and global markets.

The FII is a close-ended fund that by pooling investors’ money to invest like a condominium in various segments of the real estate market such as offices, shopping centers, hotels, residence, logistic complex. This type of fund can also invest in securities.

Which assets can a FII hold?

FIIs can invest in:

• real estate rights on real estate property; and

• fixed income securities (CRI, LH, LCI, among others); and

• FIIs cannot invest in derivatives except for the purposes of asset protection.

Summary Flowchart

Overview

The Fund Bylaws shall contain the main characteristics of the FII, including relevant information for investors about investment policies, risks involved, as well as quotaholders’ rights and duties. It shall contain at least the required elements listed below:

• Service providers as applicable;

• Target audience: A description of the target audience of the FII;

• Investment policy: Description of how the FII aims to achieve its investment goal, identifying the sectors in which it will operate, the nature of the investments that the FII will be allowed to make, i.e., the type of investments (real estate or financial assets) that will compose the portfolio;

• Investment concentration policy, when applicable: description of the investment diversification requirements and the asset selection and allocation policies;

• Amortization (when applicable) and payout policies: information about deadlines and payment terms;

• Share/Quotadescription: description of the different classes of quotas, whenever applicable, with the rights granted by each of them;

• Indication of any possible conflicts of interest: describe any possible conflicts of interest that may exist in the FII, pursuant to current legislation, and include them as risk factors in the Bylaws;

• Risk factors: indicate any and all facts related to the FII that may significantly affect prospective investors’ decision to purchase the FII’s quotas.

In addition to the regular Fund’s expenses, the FII can have the following expenses:

• commissions and fees paid on operations, including expenses related to the purchase, sale, acquisition or rental of properties;

• fees and expenses related to the activities provided for: (i) specialized consultancy, which aims to support and subsidize the activities of analysis, selection, monitoring and evaluation of real estate projects and other assets integrated or that may become part of the asset portfolio; and (ii) specialized company to manage the leases or properties, the exploration of surface rights, and monitor projects and the commercialization of the respective properties and consolidate financial data selected; and

• expenses necessary for the maintenance, conservation and repairs of properties forming part of the FII’s assets.

Best Practices for Conflict of Interest

Managing conflicts of interest (“COI”) in the fund management is crucial for ensuring integrity, and ethical decision-making. COI between FII and the administrator, manager or specialized consultant depend on prior, specific and informed approval by the Quotaholder Meeting. Examples of conflict of interest situations:

• the acquisition, leasing, rental by the FII of property owned by the administrator, manager, specialized consultant or people linked to them;

• the sale, acquisition or rental of FII property with the administrator, manager, specialized consultant or people linked to them as counterparty;

• the acquisition, by the FII, of property owned by developers from the administrator, manager or specialized consultant, once the debtor has defaulted;

• the hiring, by the FII, of people linked to the administrator or manager to provide specialized consultancy services; and

• the acquisition, by the FII, of securities issued by the administrator, manager, specialized consultant or persons linked to them.

General Advantages

• Negotiation stands out as a significant advantage in the context of FII shares compared to real estate transactions. Unlike the intricate and financially demanding nature of real estate dealings, FII shares are traded in a well-organized over-the-counter environment or on the Stock Exchange. This not only results in lower brokerage costs but also alleviates the burden of taxes associated with real estate transactions. The latter often entails extensive documentation and analysis, making it a more time-consuming process.

• The quality and management of real estate assets further contribute to the appeal of FII investments. FIIs boast professional management with dedicated teams overseeing properties that may not be readily accessible to the general public. This professionalism extends to the regulatory sphere, providing investors with a secure and transparent environment. In contrast, real estate transactions lack the same level of professional oversight, making FII investments a more streamlined and secure avenue for those seeking financial growth.

Tax Advantages

Foreign investors that (i) are not residents of a tax haven jurisdiction, and (ii) their investments are made in accordance with Central Bank regulations (Resolution nº 4373):

• 15% income tax withholding on FII distributions; and

• 15% capital gains tax on the sale or other transfer of FII quotas.

To foreign investors that are residents of a tax haven jurisdiction – same rate of Brazilian entities (20%).

In any case upon amortization or redemption of their quotas, and only to the extent that the amount amortized or redeemed exceeds the subscription price of the quotas.

Important: The FII must distribute at least 95% of the Fund’s earnings in the six-month period, calculated under the cash regime, in accordance with Law 8.668/93. Please note that if it proves unattainable on the designed structure, an alternative option is to consider a Real Estate FIP. In this scenario, the properties would be owned by the company in which the FIP has invested, limiting the ability to acquire additional real estate securities.

As a rule, foreign investments in Brazil must be registered with the Central Bank of Brazil (“BACEN”). Registration of foreign investments may be divided into two main categories: (i) foreign direct investments which are regulated by Law 4,131 of 3 September 1962, as amended, ("Direct Investment" and “Debt Transactions”); and (ii) investments made in the Brazilian financial and capital markets, which requires the use of a local custodian to represent the foreign investor, regulated by CMN Resolution 4,373[1] ("Indirect or Portfolio Investment").

The registration of foreign capital is done at the Electronic Declaratory Registration System (“RDE”), at the Central Bank of Brazil (“BACEN”) information system (“SISBACEN”).

The foreign capitals are registered in specific modules, according to their classification, which are:

- Foreign Direct Investment (“IED”);

- Foreign Debt Transactions, such as loans, long-term imports financing and royalties’ contracts (“ROF”); and

- Indirect or Portfolio Investments.

Direct Investment

According to the BACEN, a direct investment is defined as such by its intention to remain long-term in the country and by its acquisition over-the-counter markets, direct in non-listed companies[2].

Brazilian companies can receive foreign direct investment from both Individuals and Legal Entities that are not resident in Brazil.

Registration of a foreign direct investment must be submitted electronically to the Central Bank by the company receiving the investment (the investee), using the SISBACEN for direct foreign investments (“RDE-IED”).

Debt Transactions

Foreign debt transactions may be made through the exchange of foreign currency (i.e., loans, certificates of deposit, private debentures, etc.) directly between a foreign and a domestic party.

A foreign debt transaction must be registered with the BACEN before the actual inflow of funds and submitted electronically by the investee using the SISBACEN for foreign debt transactions (“RDE-ROF”). This electronic registration does not require preliminary approval.

Indirect Investments or Portfolio Investments

Investments by foreign investors in Brazilian financial and capital markets are regulated by the National Monetary Council (the "CMN"), the Brazilian Securities and Exchange Commission (the "CVM") and BACEN. The main regulation governing such investments is CMN Resolution 4,373 of 29 September 2014.With certain exceptions, foreign investors may invest in the Brazilian financial and securities markets using the same fixed-income instruments (i.e., notes, certificates of deposit, bonds and debentures), derivative instruments (i.e., swaps, futures, NDF and options), securities, mutual funds, private equity and other investment funds, and other financial instruments available to Brazilian residents.

To invest in the Brazilian financial and securities markets, a foreign investor must:

- appoint an agent in Brazil (which must be a financial institution or an institution authorized by the BACEN);

- register with the CVM; and

- enter into a custody agreement with a financial institution authorised to provide custodian services, in accordance with CVM Instruction 560 of 27 March 2015, as amended[3].

In recent years, several operational measures have been implemented to make operational foreign investment flows simpler and speedier. In this regard, almost all registration, can now be made electronically and is usually centralised in one (or more) financial institutions that provide diverse services (such as legal and tax representatives, custodians and settlement banks for FX contracts). In addition, since 2 May 2022[4], non-resident individuals will no longer be required to register directly with CVM before they can buy registered securities. Instead, his or her representative merely will be required to fill in the information on CVM’s online platform or via the exchange responsible for the market where the securities are traded.

For more information, contact Giovanni at giovannicataldi@hotmail.com and Andrea at asano@efcan.com.br.

________________

Disclaimer

The content in this article is for informational purposes only and should not be construed as financial advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by Giovanni Cataldi, Andra Sano Alencar, Finance Monthly or any third-party service provider.

[1] https://www.bcb.gov.br/rex/legce/Ingl/Ftp/Resolution4373.pdf [2] Note that there are some activities that are not allowed or that there are some restrictions. [3] ttps://www.b3.com.br/data/files/CC/B5/C0/38/43473610B4199636790D8AA8/ICVM%20560%20-%20english%20version.pdf [4] CVM Resolution nº 64, of February 7, 2022

Receivable Investment Fund (Fundo de Investimentos em Direitos Creditórios or FIDC) is one of the most common structures in Brazil for creating asset-backed securities (ABS). Created in November 2001 by Resolution 2.907 of the Brazilian Monetary Council and further regulated in December 2001 by Instruction 356 of the CVM, FIDCs are mutual investment funds that apply the majority of their financial resources (at least 50% of their net assets) in receivables (as defined by Instruction 356) of almost any kind or nature.

On 8th December 2006, CVM issued Instruction 444 providing for ‘non-standardised FIDCs and allowing the securitisation of high-risk receivables.

Since their creation, FIDCs have caused a revolution in the factoring industry in Brazil. Attracted by the operational and mainly tax advantages offered by the securitisation vehicle, many major factors have structured their own FIDCs and have carried out numerous activities through them.

FIDCs can be structured as either open- or closed-end funds. The redemption of quotas is allowed in an open fund, while in a closed-end fund, it is only allowed at the end of the term of validity of the fund.

Since their creation, FIDCs have caused a revolution in the factoring industry in Brazil.

A two-tier senior/subordinated quota is the typical structure adopted thus far, but alternative arrangements as Senior/Mezzanine/Subordinated are also allowed. They are often rated by rating agencies based on the competence of the portfolio manager and credit support derived from a senior-subordinated structure.

The FIDC offers the following advantages compared to the traditional factoring structure:

- Regulation by CVM - Despite their importance to the economy, factoring activities still lack specific laws and regulations in Brazil. On the other hand, FIDCs are fully regulated and monitored by the CVM;

- Collateral or Payment Guarantee – unlike factoring, FIDCs can require from the assignor of the receivable any kind of payment guarantee that is deemed appropriate (“coobrigação” or a third-party guarantee or collateral).

- Access to investors - due to the protection to investors conferred by regulations, it is easier for a FIDC to raise capital to fund its operations than it is for a traditional factoring business; and

- Liquidity - Although at present, the market for FIDC quotas is not very liquid, quotas of a FIDC can be listed for trading on the stock exchange or over-the-counter markets. Hence, liquidity is expected to increase as more investors become attracted to this kind of investment.

The following tax rules apply to foreign investors who are not residents of a tax haven jurisdiction and whose investments are made in accordance with Central Bank regulations (Resolution no. 4.373/2014):

▪ 15% income tax withholding on FIDC distributions; and

▪ 15% capital gains tax on the sale or other transfer of FIDC quotas.

Foreign investors who are residents of a tax haven jurisdiction are charged the same rate as other Brazilian entities.

Giovanni can be contacted at giovannicataldi@hotmail.com.

Andrea Sano contributed to this article.

Together with its subsidiaries, Helbor Empreendimentos S.A. develops and sells residential and commercial real estate properties in Brazil.

Campos Mello (in cooperation with DLA Piper) advised Marriott International on the drafting, review and negotiation of all agreements. The team included Partner Rafael Jordão Bussière and Senior Associate Ana Beatriz Barbosa Ponte.

PMKA Advogados advised Helbor Empreendimentos S.A, with Sérgio Kawasaki, Rafael Gobbi and Igor Barros.

The study, which looks at cash and cashless technology usage in four markets—the UK, Australia, Brazil, and South Africa—shows that a cashless society may not be a realistic ambition. In fact, the survey revealed an “immovable” 24% of consumers who will never abandon cash—no matter what technological advance or leap forward is available to them.

In Brazil and South Africa, where cash use is more common, there is a strong desire for wider acceptance of cashless technologies such as payment cards and digital wallets. In both markets, 60% say that they are worried about having cash stolen from them which suggests fear of theft is a key driver rather than convenience.

In the UK and Australia, however, where the use of cashless technologies is more widespread, people are happier with their use of cash. Around 80% of people in both markets say that they are comfortable using cash.

Respondents across all countries saw cash as part of their day-to-day lives. They carry cash at all times, replenishing their wallets and purses regularly at ATMs, and are unwilling to go that last extra mile and never use cash again.

The findings suggest that cashless technologies will not replace cash completely; instead people are happier with an equilibrium between the two.

“While the proliferation of cashless payment technologies has generally led to a reduction in cash usage across developed economies, banknotes have unique properties that consumers value, such as security against fraud,” said Michael Batley, Head of Strategy, Travelex. “As long as this is the case it’s unlikely that any attempts to abandon cash completely will succeed. Even Sweden’s bid to go cashless, touted as a successful model, has seen pushback. Ultimately, only consumer demand will drive the change towards a truly cashless society and our research indicates this is further away than many realise.”

As well as revealing a lack of appetite for a cashless society, the study also reveals that opinion is split on whether it is even possible. The UK, the most ‘cashless’ country surveyed, represented the highest proportion (47%) of respondents that do not see an end to cash, closely followed by Australia (42%).

Travelex commissioned Sapio Research to survey 1,000 consumers regarding their attitudes to cash and cashless technology across four markets: the UK, Australia, Brazil and South Africa. These four countries are at different points in the “journey towards cashlessness”, as defined by Mastercard’s Measuring progress toward a cashless society report, and together give a representative overview.

(Source: Travelex)

So if you clicked this article because you want to know how much the literal world cup trophy costs, it’s currently estimated at a total $10 million, or in fact more than two human figures cast in 18 carat gold, but that’s not what this is about.

For the consumers, the ticket prices alone are eye-watering. Standard category tickets for the knockout stage matches set fans back around £2,458 ($3,249), while the group stages will have cost £2,631 ($3,477) combined. All in all, that’s around 22% of the UK’s average annual salary. Plus, flights at anywhere between £600 ($793) and £1,500 ($1,983) depending on where you are in the world, insurance at £41 ($54), and hotels at around £987 ($1,305) and counting, the cost of the world cup is a small fortune for any individual fans attending the competition.

However, the true cost of the world cup extends far beyond what most can imagine. If you take into account the cost on the host nations, the funds handled by FIFA and national football associations, the money lost in advertising, operations, infrastructure and accommodating resources for businesses worldwide, from an economic perspective the overall break-even after losses and profits is highly questionable.

This year companies in the UK witnessed a blackout the morning after some of the England games; employees just didn’t turn up to work. The estimated loss figure for employees ‘pulling sickies’ reaches £500 million ($661 million) nationwide. After the England Vs Columbia game, millions of football fans were expected to call in sick, and they did. While each individual case may seem like nothing much, all together, a £500 million loss in a day is a big hit for the economy. Realistically, other football fanatic nations may have suffered a similar fate the day after their respective teams played.

But the real cost of the world cup extends much further still, and its biggest catalyst, hosting the 32-nation tournament, touches a sensitive socioeconomic nerve. While the surge of a national team in the tournament can bring a much-needed economic boost, £2.6 billion is expected to flood into the UK economy should England reach the final on July 15th, the true cost of the World Cup is always counted in billions and can cause significant issues for the host country.

The 2014 world cup in Brazil was forecast to positively impact economies anywhere between $3 billion to $14 billion. The positive economic impact of the 2010 world cup in South Africa was estimated at $5 billion; the 2006 world cup in Germany at $12 billion and the 2002 world cup in Japan & South Korea at $9 billion. The 2014 brazil world cup was due to add an estimated $30 billion to Brazil’s GDP between 2010 and 2014.

From TV rights fees to sponsorships and ticket sales, FIFA made $4.8 billion in revenue from the tournament in Brazil, with an expense of $2.2 billion, most of which comprised funding to teams and TV production costs. $100 million of the expense was the legacy payment given to Brazil. This did not however cover the costs of building and renovating 12 stadiums and developing the appropriate transport infrastructure needed to host the world cup. The overall cost of this has been estimated at around $15 billion, most of which was public funded.

On top of this further costs incurred due to overruns, legacy concerns and missed constructions deadlines. Some of the stadiums remained unfinished or untested prior to the launch of the 2014 event. In addition, many protests erupted throughout the country calling out the troublesome impact of the world cup on day to day living in Brazil, from the way public transport was handled to the way policing was affected.

The harsh truth is that many of those stadiums remain unfulfilled and unused now. Sure, they were put to good use during the world cup in 2014, but in 2018 these stand desolate, while basic social services are underfunded and lack the capital for development. Billions in capital that could have not been spent on the world cup. One of the 12 stadiums built is the Arena da Amazônia in Manaus. Situated in the middle of the jungle, without a proper top-flight football team, a 45,000-seat stadium is unnecessary. In order to build this stadium, some parts had to be transported by boat through the Amazonian jungle.

To add to the frustration of Brazilians that year, their world cup team suffered a crushing 7-1 defeat against the Germans in the semi-finals.

After being selected to host the 2018 world Cup back in 2010, Moscow has aimed for Russia to stand out as a global superpower and host the world cup in order to benefit from a big economic boost in the long term. The results of the latter are still to be seen, though in terms of media coverage and PR, Russia has been doing pretty well, with many global fans claiming that from a social and economic stand point, Russia is a far better nation than most believe it to be.

We’re currently just past the half way line in the 2018 Russia world cup and the cost is already mounting. The overall cost of Russia hosting the world cup is reported at $14.2 billion, making it the most expensive in history thus far. Russian media channels report that most of this cost consist of repairs and renovation to existing airports and transport systems as well as building 12 new stadiums, 11 new airport terminals, 12 new roads and three new metro stations in the run up to the competition. To support these, further infrastructure such as hospitals, power stations, and hotels were also injected with cash. Clearly, Russia thought it had better odds than Brazil when it came to the long-term economic advantages of hosting the world cup.

In terms of sponsorships, of 34 potential slots offered by FIFA for the 2018 world cup in Russia, 19 were filled, mostly by Russia themselves, and China (despite not even having a team in the tournament) and Qatar. KPMG currently estimates sponsorships have made FIFA over $1.6 billion. Statista has estimated around 1,000,000 foreign fans to attend the games from the first kick off to the final whistle, with a further 2 million domestic fans in the mix. FIFA says around 98% of tickets were sold, but this hasn’t always appeared to be the case in some matches.

Once the world cup is over, it’s difficult to say whether Russia’s massive investment, the biggest yet, will reap long lasting benefits from hosting the competition. But if Brazil is to be an example, probably the worst of many, then Russia is arguably set to lose from the deal, at least financially. Although the injection of cash means they will have a few more hospitals and better airports in the long term, from a future football perspective the stadiums that were purposely built for the world cup will likely not bring much revenue back for Russia in years to come, leaving the expenditure as a substantial one-off outlay, albeit it for a very rich country.

At least high hopes still remain for the Russian football team in the 2018 world cup, as they face Croatia this Saturday in the quarter finals. If they win, maybe things will look a little brighter.

Sources: https://www.vanquis.co.uk/the-cost-of-the-world-cup-2018 http://www.cityam.com/288622/cost-football-coming-home-england-fans http://theconversation.com/hard-evidence-what-is-the-world-cup-worth-27401 http://uk.businessinsider.com/fifa-brazil-world-cup-revenue-2015-3 http://www.businessinsider.com/brazil-world-cup-stadiums-2014-6?IR=T https://www.theguardian.com/world/2013/jun/18/brazil-protests-erupt-huge-scale https://www.bbc.co.uk/sport/football/30642071 https://www.cambridge-news.co.uk/news/uk-world-news/people-sickies-work-world-cup-14864331 https://www.fool.com/slideshow/games-cost-russia-14-billion-9-wild-world-cup-money-stats https://www.forbes.com/sites/jamesrodgerseurope/2018/07/02/world-cup-2018-wins-for-russia-on-and-off-the-field/2/#7cab1dfb1e3b https://uk.reuters.com/article/uk-soccer-worldcup-col-eng-penalty/this-time-england-left-nothing-to-chance-in-shoot-out-idUKKBN1JU1T6 https://www.bbc.co.uk/news/business-44711254

JPMorgan Chase & Co. and Omidyar Network announced a $10 million (€9.3 million) combined investment in FIRST, a private equity fund focused on serving the needs of low-income and underserved populations in Brazil, in mid-March.

JPMorgan Chase & Co. and Omidyar Network announced a $10 million (€9.3 million) combined investment in FIRST, a private equity fund focused on serving the needs of low-income and underserved populations in Brazil, in mid-March.

The fund will make investments in high-growth companies in sectors providing essential products and services to low-income households, such as education, healthcare, housing and financial services.

"This investment reinforces Brazil as a JPMorgan Chase focal point, regionally and globally," said Jose Berenguer, Senior Country Officer for Brazil, JPMorgan Chase. "Investing in businesses such as FIRST is the best way to contribute to Brazil's development and improve income distribution in our country."

The fund, which has raised $66 million (€61.4 million), brings together several leading global investors including the International Finance Corporation (IFC), German development finance institution DEG and French development finance institution PROPARCO to accelerate the growth of impact investments in Brazil, which seek to generate financial returns while making a positive social and environmental impact.

"Omidyar Network is pleased to support FIRST. It serves as a cornerstone of the growing impact investing industry in Brazil and brings with it seasoned venture capital expertise with a proven track record," said Eliza Erikson, Director, Investments at Omidyar Network.