Cash Budgeting: Does the TikTok Method of Using Cash Really Help You Manage Money?

In today’s digital world, where online payments, credit cards, and mobile apps dominate, using cash for budgeting might sound outdated. However, a growing trend, particularly popular on TikTok, suggests that going back to basics by taking out cash each month can help manage personal finances and reduce overspending. This cash budgeting method, often referred to as the "cash envelope system," aims to simplify budgeting and remove the temptation of overspending.

But does this TikTok cash budgeting method really work? Let’s break down how this technique can help you manage your money and whether it's the right solution for your financial goals.

What Is the Cash Budgeting Method?

The cash budgeting method involves withdrawing a set amount of cash at the beginning of the month, based on your monthly budget. You divide the cash into different categories, such as groceries, entertainment, bills, and savings, using envelopes or dividers to separate each category.

Here’s how it works:

- Set a Monthly Budget: The first step is determining your monthly expenses. This includes fixed costs like rent or mortgage, utilities, and variable expenses such as groceries, dining out, and entertainment.

- Withdraw Cash: Once you’ve established your budget, you withdraw the exact amount of cash you plan to spend for the month in specific categories.

- Divide into Envelopes: Allocate the cash into different envelopes or compartments for each spending category. Once the cash in each envelope is gone, you’ve reached your limit for that category.

- Track Spending: Instead of swiping your card or using apps, you only spend the cash in each envelope. When it’s gone, it’s gone—this forces you to stick to the budget you’ve set.

The Benefits of Cash Budgeting

Using cash as a budgeting method offers several advantages, especially for those prone to overspending or struggling to keep track of their finances. Here are a few reasons why it might work:

- Eliminates Impulsive Spending

When using a credit or debit card, it’s easy to lose track of how much you’re spending. With cash, once you’re out, that’s it. This physical limitation helps prevent impulse purchases and encourages you to prioritize what you really need.

You can find more ways to stop impulse buying here.

- Helps Build Financial Discipline

The tactile nature of handling cash makes you more aware of how much money you’re spending. Seeing your cash supply dwindle can motivate you to stick to your budget and think twice before making non-essential purchases.

- Improves Budget Awareness

Using cash forces you to be more intentional about your purchases. It encourages you to plan and stick to your budget categories, which helps you understand exactly where your money is going each month.

- Reduces Debt Accumulation

Because you’re not using credit cards, the risk of accumulating more debt is significantly reduced. The cash budgeting method keeps your spending within your means, preventing you from racking up credit card balances that could lead to financial trouble.

Does the Cash Budgeting Method Really Work?

While the cash budgeting method can help many people, especially those who need strict controls to avoid overspending, it may not be the best option for everyone. Here’s a look at some of the downsides and challenges of using cash to budget.

- Inconvenient for Larger Purchases

In today’s world, many purchases, such as online shopping or larger expenses like plane tickets, require a debit or credit card. Carrying large amounts of cash can also be inconvenient or even unsafe in certain situations.

- Lack of Rewards

Many credit cards offer cashback, points, or other rewards for everyday spending. By relying solely on cash, you miss out on these potential benefits, which could lead to long-term savings if used wisely.

Find a reward credit card. - https://www.finance-monthly.com/2024/10/best-credit-cards/

- Harder to Automate Payments

For bills that are automatically deducted from your account, such as utilities, subscriptions, or mortgage payments, using cash can make it harder to manage payments. You’ll need to be vigilant about withdrawing cash and paying bills manually, which could lead to missed payments if you’re not organized.

How to Save Money with the Cash Budgeting Method

If you're considering adopting this cash-based budgeting system, here are a few tips to help maximize your savings:

- Set Realistic Budgets

It’s essential to create a budget that reflects your actual needs and spending habits. Don’t set unrealistically low amounts in each envelope, as this may lead to frustration or overspending when you run out of cash prematurely.

- Track Your Spending

Even though you're using cash, it’s still important to track your spending regularly. Keeping a record of how much you’ve spent in each category allows you to adjust future budgets and avoid overspending.

- Cut Back on Non-Essential Categories

The physical nature of cash makes it easier to visualize where your money is going. Use this awareness to identify where you can cut back, such as reducing dining out or impulse purchases, and allocate more towards savings.

- Use Leftover Cash Wisely

If you have leftover cash in your envelopes at the end of the month, don’t simply spend it. Consider moving the extra money into a savings fund or investing it to grow your financial security.

- Take Advantage of Digital Tools

While the cash system is low-tech, you can complement it with budgeting apps like YNAB (You Need A Budget) or Mint to track your overall financial goals. This hybrid approach can help ensure you stay on track, especially for bills and expenses that aren’t paid with cash.

Budgeting apps can help you save and keep you to your goals.

Is the Cash Budgeting Method Right for You?

The cash budgeting method, popularized on TikTok, can be an effective tool for those struggling with overspending and looking for a tangible way to stick to a monthly budget. It offers simplicity, transparency, and accountability by forcing you to manage money without relying on credit cards or digital transactions.

While this method may not be ideal for every aspect of personal finance, especially for larger purchases or online payments, it can serve as a helpful foundation for better spending habits. If you’re looking to regain control over your monthly spending, trying out the cash budgeting system may be a step in the right direction.

UK Housing Market Sees Homes Selling Quicker in October 2024

The UK housing market has experienced a notable uptick in activity this October, with houses selling quicker than in previous months. According to data from property platform Rightmove, the number of homes sold in October 2024 has increased by a third compared to the same time last year. This surge in demand is driven by several key factors, including improved market confidence, more realistic pricing by sellers, and an easing of mortgage rates. As a result, homes are moving off the market faster, signaling a more competitive environment for buyers.

Boost in Buyer Confidence

One of the driving forces behind the faster sale times is a renewed sense of confidence among buyers. The economic uncertainty that gripped much of 2023 has somewhat stabilised in 2024, allowing prospective homeowners to re-enter the market with greater assurance. The lingering impacts of inflation and cost-of-living increases have moderated, and while the economy remains cautious, there's less fear of drastic interest rate hikes.

This resurgence in market confidence has led to an increased number of buyers looking to capitalise on relatively stable conditions. The housing market is traditionally slower toward the end of the year, but the increased activity in October reflects a change in the typical seasonal pattern. Buyers seem eager to make purchases before any potential changes to mortgage rates or economic conditions in the months ahead.

Easing Mortgage Rates Boost Demand

Another significant factor driving the quicker sale of homes is the slight relaxation in mortgage rates. After a period of high interest rates in response to the inflation surge in 2023, rates have started to ease in 2024. While mortgage rates are still higher than in the low-interest years of the pandemic, the market has seen a dip that makes borrowing more manageable for potential buyers.

With mortgage rates coming down, buyers are better able to secure financing for property purchases. This is especially relevant for first-time buyers and those looking to remortgage, as they now have more flexibility to act quickly. The increased affordability of mortgages has contributed to a rise in property demand, pushing homes to sell at a faster pace as buyers seize the opportunity.

Mortgage rates are predicted to continue falling in 2025. -

More Realistic Pricing from Sellers

Sellers have also played a key role in driving the quicker sale of homes by adjusting their expectations. During 2023, many sellers held onto unrealistically high prices, believing that the market would continue to favor them. However, the slower market conditions earlier in 2024 forced a reevaluation, with many sellers now pricing their homes more in line with market trends.

This shift in pricing strategy has made properties more attractive to buyers. The combination of realistic pricing and the desire to close deals quickly before year-end has created a perfect storm, with homes selling faster than anticipated. Sellers are becoming more willing to negotiate and settle for prices closer to the asking price, leading to quicker transactions overall.

Regional Variations in Sale Times

While the overall trend points to homes selling faster across the UK, there are regional variations in how the market is performing. Major cities such as London, Manchester, and Birmingham have seen particularly high levels of demand, pushing sale times down significantly. In these areas, the competition for properties is fierce, and homes are often being snapped up within days of hitting the market.

You can see the most expensive places to buy a home in the UK here.

On the other hand, more rural areas and smaller towns are experiencing a steadier, though still positive, increase in sales activity. These regions have also benefited from the easing of mortgage rates and improved pricing strategies, though the demand isn't as intense as in urban centers. As remote work remains a viable option for many, there is still a steady interest in properties outside of major metropolitan areas, contributing to quicker sales nationwide.

Impact of New Housing Stock

Another factor contributing to the quicker sale of homes is the availability of new housing stock. Several new developments have come to market in 2024, adding fresh inventory at a time when demand is high. These new builds, which often come with energy-efficient features and modern amenities, are especially attractive to buyers who may be concerned about future utility costs or the need for costly home renovations.

The addition of new housing options also helps reduce some of the bottlenecks in the market by offering a wider variety of homes to choose from. This diversity in housing stock, combined with competitive pricing and mortgage accessibility, is helping to speed up transactions as buyers find homes that meet their needs more easily.

The Role of Buy-to-Let Investors

Buy-to-let investors are also playing a role in the quick turnaround of property sales. With the rental market remaining strong, many investors see the current housing market conditions as a prime opportunity to expand their portfolios. Lower mortgage rates and the potential for long-term rental income make it an appealing time for landlords to purchase additional properties.

As a result, buy-to-let investors are snapping up homes that are suitable for renting, contributing to the overall speed at which properties are being sold. This has been particularly noticeable in cities with high demand for rental properties, where investors are keen to secure homes before the market becomes more competitive.

Outlook for the Rest of 2024

Looking ahead, the trend of homes selling faster is expected to continue, especially as we move into the final months of the year. Buyers are eager to finalise purchases before any potential economic changes, and sellers are motivated to close deals before the holiday season slows down activity.

However, experts caution that the market may face some uncertainty in early 2025, depending on how interest rates and inflation evolve. While the current environment is favorable for quick sales, any shifts in these key factors could influence how the housing market performs in the near future.

In summary, October 2024 has seen a notable increase in the speed at which homes are being sold across the UK. Improved market confidence, easing mortgage rates, and more realistic pricing from sellers have all contributed to this surge in activity. As the housing market adapts to these conditions, both buyers and sellers are benefiting from quicker transactions, making this an exciting time for the UK property market.

Investing strategies for your 30s

When you reach your 30s, investing is a great way to expand your finances and make sure you are doing everything you can for your future. If you have already started, then there could be ways to improve your investment strategies. If you are a beginner investor in your 30s then this will help you find the strategies for you.

If you are a beginner to investing, then you can find out how it works here.

A study by robo-advisor Personal Capital found that the average age people begin investing is 33.3 years. It’s important to understand that starting now can significantly impact your financial future. The earlier you start investing, the more time your money has to grow through the power of compound interest. Compounding can exponentially increase your returns over time, making it one of the most effective strategies for wealth accumulation. Use our compound interest calculator.

Your 30s are a pivotal time to establish or refine your investment strategies. By understanding your limits, seeking diversification, clarifying your goals, considering homeownership, investing in stocks with just a little risk and committing to regular reviews, you can create a strong financial foundation for your future. Starting now will set you on the path to achieving your financial aspirations, no matter when you begin.

So, take a look at some key investing strategies for your 30s.

Check out Investing strategies for your 20s.

Investing Strategies for Your 20s

Investing in your 20s can seem daunting, but it's one of the best ways to build wealth for the future. The earlier you start investing, the more time your money has to grow. If you are interested in beginner investing then you will need to take a look as these effective strategies you can start using to make your financial planning easier. This will help you understand how to start investing, it's never too late to start but the earlier you can, the better so you can maximize your return.

Here are 7 effective investment strategies tailored for your 20s.

The Importance of Retirement Planning

Retirement planning is crucial for your financial stability in your later years, as you will have to sustain your lifestyle without a regular income. If you must rely on the state pension, this can lead to a challenging financial situation. By beginning your retirement planning as early as you can, you are giving yourself the best chance later on.

Learn more about state pension.

Find out below how much you should have already saved for retirement based on your age group and what strategies you can put in place today to keep up!

Overview of Average Savings for Retirement

In the UK, many individuals struggle to save adequately for retirement. The average retirement savings can vary significantly based on factors such as income level and age. Generally, it’s recommended that individuals aim to save at least 15% of their salary annually to achieve a comfortable retirement. However, many fall short, often relying on state pensions, which may not provide sufficient income to maintain their desired standard of living.

Impact of Age on Savings Strategies

Age plays a vital role in shaping retirement savings strategies. If you can start putting money away for retirement as you begin to enter full-time work, you will be able save much more. The amount you save each year can also increase as you earn more overtime and are able to manage your finances. As people begin approaching retirement age, their risk tolerance also decreases meaning that the return can often be limited.

If you are thinking about beginning your retirement planning, no matter your age, it is never too late to start, get saving now and live your best life during retirement!

Statistics on Average Savings by Age Group

In the UK, average pension pots vary significantly across different age groups. Use this as your guide so you know what to aim for. Despite this being what others similar to you might have saved, the amount you need to save for retirement is a lot more!

As of recent data:

Under 30s: The average pension pot is approximately £8,000. Many in this age group are just starting their careers and may not be prioritising pension contributions.

Ages 30-39: The average rises to about £32,000. Individuals often begin to focus more on savings as their careers progress.

Ages 40-49: The average pension pot increases to around £77,000, reflecting a growing emphasis on retirement planning.

Ages 50-59: The average jumps to approximately £125,000, as many are actively preparing for retirement.

60 and over: The average pension pot for this group stands at about £190,000, though this can vary widely depending on individual circumstances and retirement plans.

You can also find out the average savings based on age so you can find out if you are on track.

Factors influencing average retirement savings:

Income Levels: Higher earners typically save more, contributing to larger pension pots. Conversely, lower-income individuals often find it challenging to save adequately. This is true for private pension pots as well as workplace pensions as your salary will decide how much is put into your pension pot.

Lifestyle Choices: Personal spending habits can significantly affect how much individuals are able to save. Those who prioritise long-term financial security may allocate more towards their pensions.

Employment History: Career stability and job changes can impact savings. Individuals with consistent employment often have more opportunities for pension contributions, while those with gaps in employment may struggle to build adequate savings.

Financial Literacy: Understanding the importance of retirement savings and investment options plays a crucial role. Individuals who are more informed about pensions tend to save more effectively. This is why learning effective ways to save for retirement is so important. The more you know, the more you can help yourself.

Importance of Having a Personalised Savings Target

Having a personalised savings target is essential for effective retirement planning. It allows individuals to set realistic goals based on their unique circumstances, including income, lifestyle aspirations, and retirement age.

Having a tailored approach will help you assess how much you need to have saves to achieve your desired retirement outcome.

Find effective ways to save for retirement.

How Much Money Do You Need to Retire at Age 60?

When you are planning your retirement funds it can be effective to determine your potential expenses. This way you will know what you are saving for. During your retirement it is expected to spend about 70-80% of your pre-retirement income annually.

For the minimum retirement living standard from reports from 2019 is £10,900 for a single person and £16,700 for a couple according to Standard Life. Since 2019 this would have increased around £700 and £1000 respectively.

For a comfortable lifestyle during retirement which includes several luxuries such as, holidays and financial freedom will cost on average £33,600 for a single person. This would be £49,700 for a couple which would have increased since 2019 by an estimate of £2,200.

The key expenses include;

- Housing Costs: This can include mortgage payments, property taxes, and maintenance. On average, retirees may allocate around £12,000–£15,000 per year for housing. The amount spent on this will depend on location and type of property.

- Healthcare Expenses: As individuals age, healthcare costs typically increase. Estimates suggest retirees might spend around £3,000–£5,000 annually on health-related expenses.

- Living Expenses: Daily living costs—such as groceries, utilities, and transportation—can average around £10,000 per year.

- Leisure and Travel: Many retirees save for leisure activities and travel, with average annual spending in this area often reaching £5,000–£10,000.

- Emergency Fund: Setting aside an emergency fund of £1,000–£2,000 is recommended to cover unexpected costs.

Overall, a retiree at 60 may need approximately £25,000–£40,000 annually to maintain a comfortable lifestyle, depending on individual circumstances.

Savings strategies by age group

In Your 20s: Start Early

By starting early you can maximise the power of compound interest. Use our compound interest calculator to see how it works.

Aim to save 10-15% of your income. Consider contributing to a pension scheme, such as a Workplace Pension, where employers often match contributions. A Stocks and Shares ISA is also a great option for tax-efficient savings and investments. What is an ISA?

Tips for Budgeting and Saving Effectively

Create a budget to monitor your spending and identify savings opportunities. You can use budgeting apps to help you.

In Your 30s: Building Momentum

As your income rises, increase your savings contributions. Strive for 15-20% of your income to go towards retirement savings, taking full advantage of any employer matching in your pension.

Start diversifying your investments by including a mix of equities and bonds in your pension or ISA. This balance can help manage risk while maximising potential returns.

- Prioritise high-interest debts, such as credit cards, and pay them off as quickly as possible.

- Consider consolidating debts to lower interest rates and make repayments more manageable while continuing to save.

In Your 40s: Catching Up

Reevaluate your retirement goals and assess whether your savings are on track. Adjust your strategy as needed based on lifestyle changes, income, or shifts in retirement plans.

If possible, increase your pension contributions to the maximum allowed. Taking advantage of tax relief can significantly boost your retirement savings.

- Consider side hustles or freelance work to generate extra income.

- Look into real estate investments, such as buy-to-let properties, to enhance your financial portfolio.

In Your 50s: Preparing for Retirement

Now is the time to boost your savings. Aim to save 20-25% of your income if possible, focusing on your pension and other investment vehicles.

Evaluate your current spending and identify areas where you can cut back. This will allow you to redirect funds into your retirement savings in these crucial years.

Common Retirement Planning Mistakes to Avoid

Planning for the long-term - People often underestimate the length of time they need to save for in retirement. Planning for a longer retirement can help ensure you don’t outlive your savings.

Planning for Inflation and Unexpected Costs - Consider how inflation will affect your retirement savings. If you are just starting to save then by the time you need your retirement funds it will be worth less due to inflation. Additionally, you will need to prepare for any unexpected expense during retirement such as, home repairs.

Importance of Regularly Reviewing and Adjusting Plans

Life circumstances change, so regularly review your retirement plan. Adjust your savings strategy as needed to stay on track towards your goals.

Adapting to Life Changes

Be prepared to adapt your savings plans in response to job changes, family dynamics, or health issues, ensuring that your retirement strategy remains aligned with your current situation.

- Limit discretionary spending on non-essentials and focus on building your emergency fund.

- Automate savings by setting up direct debits to your savings or investment accounts.

Have you got enough money put away for retirement based on the statistics above? Leave a comment below

7 Simple ways you can make money now

In today’s fast-paced world, finding easy ways to make some extra cash can be a game-changer. More people are looking for ways to make extra money, at the beginning of 2024 in the UK 1 in 4 adults had a side hustle, small business or a secondary job alongside their full-time careers. In the US more than a third of adults — and nearly half of millennials and Gen Z have a second stream of income in 2024.

Whether you need to pay off bills, save for a vacation, or just have some fun money, there are numerous avenues available that anyone can tap into. Here are 7 simple ways you can make money now!

Revolut bank account – is it safe?

Digital banking provides consumers with convenience and accessibility to banking unlike traditional banks. With digital banking financial services become simpler and consumers can manage their money without the need for a physical branch. The most popular online banking platforms include Revolut, Monzo, Chase, N26 and Wise. These services offer features such as instant money transfers, budgeting tools, and cryptocurrency trading, catering to a tech-savvy audience seeking convenience and efficiency.

According to a survey over 70% of consumers prefer digital banking over traditional methods. More people are shifting to online platforms but the importance of security in digital transactions remains vital with high cases of fraud.

These online services are pulled into question again in October 2024 with Revolut in the spotlight. A Revolut customer recently lost £165,000 to fraud in just one hour, and the company’s refusal to issue a refund despite the system failing has ignited a widespread concern over customer protection with digital banking.

Now people are asking, is digital banking safe for my money?

A Recent Fraud case

A particularly alarming incident occurred recently when a Revolut customer lost £165,000 to fraud within an hour.

According to a BBC report, the individual was targeted in a sophisticated scam that involved a quick and decisive breach of their account. Despite the urgency of the situation and the significant loss, Revolut denied the customer’s request for a refund, citing their policies and the circumstances surrounding the fraud.

The customer has stated the lack of support from Revolut and the time it took to get through to the right team to freeze his Revolut bank account, meaning more money was leaving his account until they acted.

This case has prompted widespread outrage, with many questioning Revolut's commitment to customer protection. Critics argue that a digital banking account should have robust systems in place to detect and prevent fraud, as well as fair policies for refunding victims. The incident serves as a stark reminder of the vulnerabilities that exist in digital banking and the potential consequences for consumers as banking fraud become more common.

The risk of fraud in digital banking

While the benefits of digital banking are clear, the rise in online transactions has also led to an increase in fraudulent activities. Common types of fraud in digital banking include phishing attacks, where scammers impersonate legitimate institutions to steal personal information, and account takeovers, where unauthorised individuals gain access to a user’s account, in some cases this can lead to identity theft.

Banks should have systems in place to protect their customers from fraud as well as providing support after any fraud incidents.

What measures do digital banking platforms take against fraud?

To combat the rising threat of fraud, digital banks have implemented various security measures. Two-factor authentication (2FA) is one of the most common practices, requiring users to provide two forms of verification before accessing their accounts. Biometric verification, such as fingerprint or facial recognition, is also becoming standard, adding an extra layer of security.

Additionally, many banks are leveraging artificial intelligence and machine learning to enhance fraud detection. These technologies can analyse transaction patterns and identify suspicious activity in real time, allowing banks to act swiftly and prevent unauthorised transactions.

Despite these measures many banks are suffering from high cases of fraud.

Customer protection and refund rates

Customer protection policies differ significantly among digital banks, particularly when it comes to handling fraud claims. Revolut bank, for instance, has faced scrutiny for its refund practices, with critics claiming that its policies do not sufficiently safeguard consumers.

According to industry reports, traditional banks are generally more robust in their refund processes, often offering a higher rate of compensation to customers. This discrepancy raises questions about whether digital banks can maintain customer trust while competing on convenience and innovation.

Make sure you know what to do if you are a victim of fraud. It is important to act fast and protect your money.

Contacting your bank

If you suspect fraud on your account, you should try to act quickly to prevent further theft and protect your money and data. With digital banking, most apps will have a feature for you to freeze your account so the fraudster cannot take anything more out of your account. Then you should contact your bank.

By banking with Revolut you can use the app to block and freeze your card and account at any time. You can also do this by calling +442033228352.

If you are banking with Monzo and predict fraud on your account then you can talk to them on the app 24/7, call them on 0800 802 1281 or if you are outside of the UK call them using this number, +44 20 3872 0620.

If you are banking with Chase then call 08003763333 from the UK, if you are outside of the UK then call +44 2034930829. You can also contact Chase through the Chase app.

If you bank with Wise then you can log the case on the app and contact them on +44 808 175 1506.

N26 bank suggest using your app or webpage login to request blocking your card and account by calling their phone line at +44 2035 107126 or +49 303 6428 6881.

Convenience VS. Security

As digital banks continue to grow, they face the ongoing challenge of balancing user-friendly interfaces with the need for robust security measures. While consumers appreciate the convenience of instant transactions and easy access to their finances, they must also recognise their responsibility in protecting their accounts. This includes using strong passwords, being cautious about sharing personal information, and regularly monitoring account activity.

Have you ever been a victim of fraud and did your bank protect you? Leave a comment below.

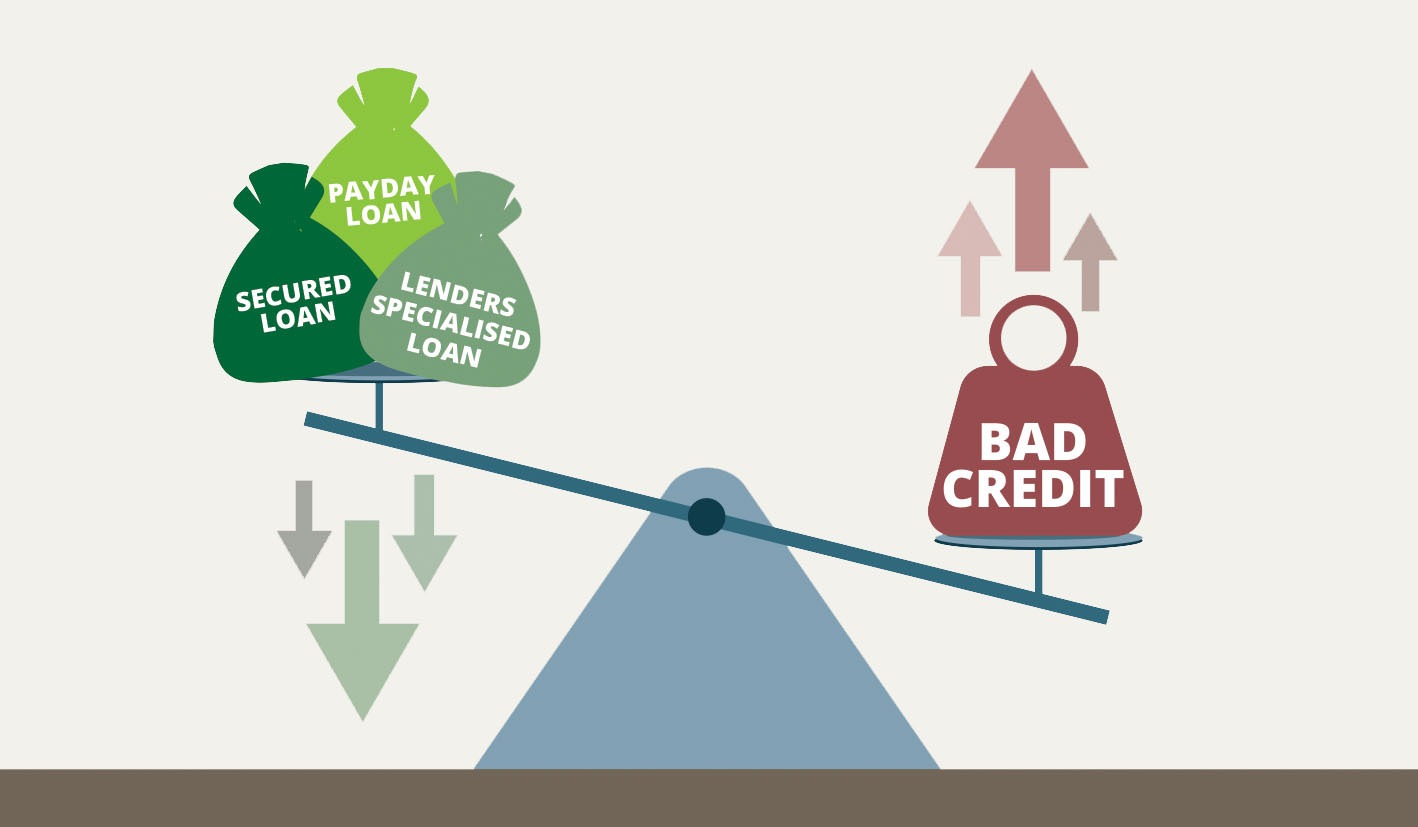

Can I get a loan with bad credit?

For those with bad credit, securing a loan can be a long battle as lenders view borrowers with a low credit score as high risk. This can often lead to stricter terms, higher interest rates or even denials. However, finding loans with reasonable terms is crucial for those with bad credit. Finding a loan with fair interest rates and manageable repayment schedules can help them cover necessary expenses without falling further into debt.

Being able to repay the loan will also provide an opportunity to improve credit scores which can then open the door to more financial opportunities in the future.

There has been a growing demand for personal loans in the US in 2024 with 93.9 million Americans currently holding personal loans.

This is a 5.3% year-on-year increase. Partly this is due to a rise in accessible loan options for those with bad credit as more lenders are offering bad-credit loans, secured loans, and alternative lending platforms. Navigating your financial choice carefully is essential to avoid high fees and dangerous lending practices.

You can take out a loan with bad credit but doing so should be carried out carefully.

What is classed as having bad credit?

Lenders will assume you are a high-risk borrower if you have a FICO score below 580. Credit scores typically range from 300-850 with higher scores indicating strong creditworthiness. Scores below 580 falls into the ‘poor’ category which then makes it challenging to secure a favorable loan.

If you miss or make your payments late on credit cards, loans or bills you will damage your credit report and could end up with a significantly lower score. High credit utilization or using a large portion of available credit will also negatively impact your score. If a borrower is unable to repay debts this will be recorded, and future lenders will be more wary.

Best loans for bad credit October 2024

When you have bad credit, finding a personal loan can be challenging, but there are several options available, including payday loans, secured loans, and loans from specialized lenders. Personal loans with a bad credit score is possible but should be carefully considered in order to avoid inescapable debt.

Payday loans

Payday loans are short-term loans designed to be repaid by your next paycheck. These loans are often marketed to borrowers with bad credit, offering quick cash with minimal application requirements. However, payday loans come with extremely high interest rates, often exceeding 400% APR, and costly fees. While they provide immediate relief, they can easily trap borrowers in a cycle of debt if not repaid on time. Payday loans should only be used as a last resort. Recent regulations in 2024 have introduced more consumer protections, limiting the amount a borrower can take and capping interest rates in some states. Still, they remain risky and should be approached with caution.

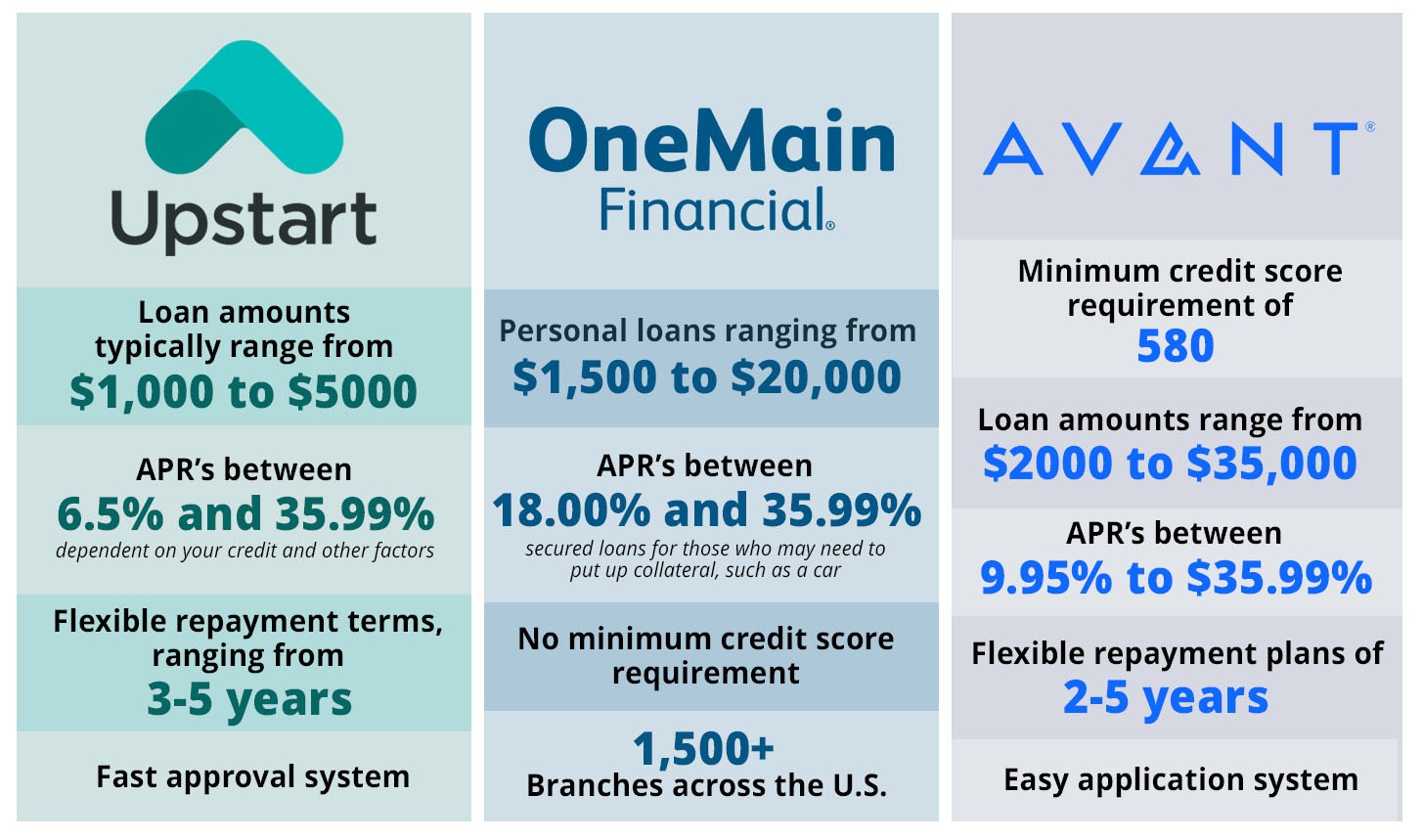

Lenders specializing in loans for bad credit

Several lenders cater specifically to individuals with low credit scores. These loans often have higher interest rates compared to those available for borrowers with good credit, but they offer better terms than payday loans. Loan amounts typically range from $1,000 to $10,000, with repayment terms usually between 12 and 60 months, depending on the lender.

In October 2024, lenders like Upstart, OneMain Financial, and Avant continue to offer personal loans for bad credit borrowers. Upstart, for example, uses a unique model that factors in education and employment, while OneMain Financial focuses on offering personalized loan terms based on your financial situation. Avant provides flexibility with repayment and has lower credit score requirements.

Secured Loans

Secured loans are another option for borrowers with bad credit, backed by collateral such as a car or home. These loans reduce the risk for lenders, making it easier for individuals with low credit scores to get approved. Common types include car title loans or home equity loans, where the borrower’s asset is used to secure the loan. The advantage is often a lower interest rate compared to unsecured loans, but the downside is the risk of losing your asset if you default on payments.

Best loan companies for bad credit

How to choose a loan for bad credit

When choosing the best loan for bad credit, understanding key criteria can help you make a smart financial decision. Here are the factors you should evaluate:

Interest rates

This is one of the most important factors when choosing a loan. Borrowers with bad credit often face higher rates, but there can be significant differences between lenders. Look for the APR which includes both the interest rate and any other associated fees. Make sure you compare rates across multiple lenders to ensure you are getting the best offer available. The lower the interest rate, the lower your monthly payments will be, this will help you repay the loan.

Fees and Penalties

Loans often come with various fees and penalties that can add up. Watch out for origination fees, which are usually deducted from the loan amount upfront. Some lenders also impose late payment penalties or prepayment penalties for paying off your loan early. Be sure to read the fine print and ask about any additional costs. Lenders who are transparent will clearly outline all fees upfront, so avoid any that seem to hide or gloss over these charges.

Repayment terms

Some loans offer shorter terms with higher monthly payments, while others provide longer terms with lower payments but higher overall costs due to interest. Consider how flexible the repayment schedule is, and ensure it aligns with your budget. Look for options that allow early repayments without penalty, especially if you plan to improve your financial situation over time.

Approval process

Some lenders offer fast approvals with minimal checks, whereas others may conduct a thorough credit check and verification process. Being approved quickly will be tempting, however they can often come with higher interest rates and fees.

Check customer feedback and reviews

During your research it is important to take a look at past customer reviews and feedback. This will tell you how trustworthy the lenders are and whether this is a good decision for you.

Alternative to loans for bad credit

If you cannot find a loan with favorable terms and you have a bad credit score, there are some other options.

Credit builder loans

They are designed to help improve your credit while borrowing money. The lender will hold the loan amount, whilst you make regular repayments. This is a way to prove you can be a low risk, trusted borrower and in the future more lenders will accept you.

Debt consolidation loans

For those with multiple debts, a debt consolidation loan can combine them into one monthly payment, often with a lower interest rate. This simplifies repayment and can reduce overall interest costs.

Secured credit cards

You will have to provide a cash deposit as collateral, this makes them easier to obtain with bad credit.

What is Statutory sick pay?

Statutory sick pay (SSP) is a legal requirement in the UK which employers must adhere to, it provides financial support to employees when they are unable to work due to illness. If employees are off work for 4 consecutive days, employers must comply with SSP.

So what is statutory sick pay and how much is it?

What is the purpose of SSP?

SSP is crucial to employees as it provides financial security and prevents job loss during illness. Employees will still receive the minimum level of income available whilst they are away sick, meaning they won’t have to worry about their finances or force themselves into the workforce.

Complying with SSP also creates a healthier workplace for staff where they can reduce the spread of illness and be assured, they have the freedom to recover. This contributes to a more productive and longer-lasting workforce in the long term.

What is the amount of Statutory sick pay?

If you working then you should know what Statutory sick pay you are entitled to and ensure that your workplace is adhering to their legal obligations.

You will be paid for all the working days you are off sick, except the first 3 working days which are counted as the waiting period. This is the amount of SSP you are entitled to in the UK.

If you are eligible, you can be paid £166.75 a week SSP for up to 28 weeks of the year.

You will be paid by your employer through the same system as your normal weekly or monthly pay. If you have multiple jobs, you may get SSP from each one.

SSP eligibility

SSP is available to those working in the UK under a signed contract. Employees are eligible for 28 weeks of SSP, if you have used this amount already, you will not be provided extra.

You must be ill for at least 3 days or more, this does include non-working days.

You must inform your employer within their set time or within 7 days if there is no set regulation on this.

You could be asked to provide an appropriate fit note to show proof of illness. This can include a printed or digital note from the GP, registered nurse, physiotherapist, occupational therapist or pharmacists.

What if my employer is not providing SSP?

As an employee, you are protected by law and employers who fail to meet SSP obligations could face penalties. If your employer is not providing Statutory Sick Pay and you believe you are entitled to it, then there are steps you can take.

First, take a look at the criteria again to confirm you are eligible for SSP, then raise the issue with your employer to ask for an explanation. If they do not resolve this themselves then you can contact HMRC for assisstance. They will investigate the situation and if your employer is in breach of their legal obligations HMRC will help you get the SSP you are owed.

SSP VS. Company sick pay

While SSP can provide the minimum level of financial support for those unable to work due to illness, some employers will offer a more generous alternative, company sick pay.

SSP is regulated by the government and there is a set amount which has to be paid to the employee if the criteria is met. However, company sick pay is a benefit offered by the individual business. This will usually cover the employee’s full salary or a higher percentage of their wages for a longer period than the SSP. The employee could receive their full salary for the first 2 weeks of illness, followed by a reduced percentage for any weeks after.

This should be outlined in your work contract as company sick pay is an optional scheme set up by the employee.

Recent updates to SSP

There are changes to statutory sick pay. The BBC have reported that stronger protection for employees surrounding sick pay will be coming into action. There have been calls over the past year to increase the current SSP rate as costs of living increase. This would better support those workers living in periods of sickness without financial support. This would also include those working on a zero-hour contract as the criteria stipulates you must earn at least £123 per week.

The government is working to improve standards including workers being entitled to SSP from their first day of sickness rather than waiting until the 4th. Additionally, they are aiming to increase the SSP rate dependent on salary.

Ministers have said that these changes to statutory sick pay would benefit around nine million workers who have been with their current employer for less than two years.

The economic impact of natural disasters in the US

For those living in vulnerable areas to extreme weather disasters, recent years have seen some of the worst disasters. In 2024, we have seen severe weather disasters such as, the floods in Afghanistan- Pakistan, typhoon in Japan, the recent hurricane in Florida and more. Now, hurricane Milton is causing severe warnings and evacuations in Florida as they still face the outcome of their last hurricane, Helene.

These disasters cause destruction to lives, families, property and more and the cost of repairing this once they can is substantial. We have taken a dive into the cost to the US economy, businesses and individuals when they are hit by a natural disaster

The cost of weather disasters in the US

Between 2020-2022 there were 60 natural disasters which cost over $1 billion in losses. With the worsening climate change, 2023 saw a record number of weather and climate disasters. In 2023, flooding events alone caused a total of almost $7 billion in damages in the U.S.

The cost of property damage and destruction of infrastructure are often the most clear and immediate impacts, as homes, buildings, roads and more are damaged or destroyed. The economic impact also extends to business interruption, loss of jobs, reduced tourism and more which lead to further financial strain.

The costs of repairing and rebuilding

Hurricane Katrina in 2005 caused an estimated $125 billion in damage, with widespread destruction to property and infrastructure across New Orleans. The storm crippled businesses and left thousands without jobs, contributing to long-term economic stagnation in the region. Housing markets are heavily impacted by property damage. After Hurricane Katrina, housing prices in New Orleans dropped significantly as many properties were either destroyed or made uninhabitable.

Not only did the storm Katrina impact infrastructure but also the essential businesses were halted. Katrina impacted up to 19% of the total US oil production as 24% of the country's natural gas supply is housed in or around areas impacted by the storm. 20 offshore rigs underwent significant damage causing refineries to halt production. This was the first time in the country’s history that the national average gas price went over $3.

Who pays for repairs?

Contributions from the government

Federal as well as local government are often the first to respond after a disaster, they will allocate money for emergency relief and reconstruction. Agencies like FEMA (Federal Emergency Management Agency) provide financial assistance to individuals, municipalities, and states to cover the cost of rebuilding infrastructure and homes. In 2027, the hurricane season brought 3 large disasters, the federal relief packages amounted to $130 billion.

At the state and local levels, additional funds are provided, though these governments often struggle to meet the demands of large-scale recovery due to budget limitations. This has led to calls for increased federal support and better pre-disaster planning.

Insurance Companies

If you are a homeowner and you have property insurance you can file claims to cover damage to homes, cars, and other possessions. Unfortunately, not all areas of the US are equally insured, such as those areas prone to specific types of disasters e.g. hurricanes and wildfires. Insurance premiums have increased the prices due to the heightened risk.

For example, after Hurricane Katrina, insurance premiums in coastal areas of the Gulf and Atlantic soared by as much as 20-30% in some regions.

Some homeowners may not be able to afford sufficient coverage, leaving them vulnerable to significant financial losses after a disaster. Additionally, many policies don’t cover flooding unless a separate policy is purchased, as seen in the extensive uninsured losses from Hurricane Harvey, where only about 20% of homeowners in the Houston area had flood insurance.

The impact on small businesses

A 2017 FEMA report highlighted that 40% of small businesses never reopen after a disaster. In these cases, both individuals and businesses are forced to rely on personal savings, loans, or government assistance, which may not be sufficient to cover the full extent of the damage.

Some of the hidden costs of weather disasters

Employment: Natural disasters can have various effects on the economy of the local area which ripple through multiple sectors. With productivity down, businesses begin to struggle and even more so if their property has been damaged or destroyed. The money to restore the business may not be immediately available, causing the owners and all staff to be without employment for a prolonged amount of time.

Housing market: When disasters hit, and if the area has been hit multiple times, it is likely to deter future residents. Currently, Florida is facing its second large hurricane within a month, this will likely persuade many to relocate and others to delay or cancel their move into the area. This will have a substantial impact on the housing market.

Investments: For investors, an area prone to natural disasters will likely deter any development in the area. This can include property investment as well as developing the area with more businesses.

The Best Rewards Credit Cards of October 2024

A rewards credit card can be a great financial tool to gain a perk from using your card and keeping on top of your finances. This only stays beneficial when you stay on top of payments and don't get behind, as you could face even higher late payment fees than a regular credit card.

Take a look at some of our picks for rewards credit cards and see the perks on offer.

Best Budgeting Apps for Families in 2024

Looking for the best budgeting apps to manage your family's finances in 2024? We’ve reviewed the top apps that make it easier to track spending, set savings goals, and take control of your personal finances. From user-friendly features to comprehensive tools, discover which app suits your needs for smarter money management.

Managing family finances can be overwhelming with all the daily expenses, savings goals, and unexpected costs that come with raising children. Whether it’s keeping track of grocery bills, school fees, or saving for a family vacation, it’s essential to have a clear and organized system. That’s where budget tracking tools for parents can come in handy. These tools offer an easy way to manage household expenses, plan for long-term goals, and ensure everyone in the family is aligned financially.

Why Families Need Budgeting Apps

Budgeting is a key tool for any household and when there are children involved this tool can become even more helpful. With multiple expenses, income streams and the need to plan for the future, keeping your finances in check can become challenging - so what best apps for household finances?

Budgeting apps are there to help you;

- Track Shared Expenses: From groceries to utilities, a budgeting app allows families to monitor how much they’re spending and on what.

- Plan for Long-Term Goals: Whether it’s saving for your child’s education, a family vacation, or a new home, apps make it easier to set savings targets and see progress.

- Manage Daily Costs: Families can stay on top of routine expenses like transportation, food, and healthcare while preparing for unexpected costs.

By using a budgeting app, families can collaborate, manage expenses in real-time, and build better financial habits together. Let’s explore some of the top budgeting apps that are perfect for families.

Best Budgeting Apps for Families in 2024

1. You Need A Budget (YNAB)

You Need A Budget (YNAB) is known for its focus on giving every dollar a job. This app allows families to assign money to specific categories like bills, groceries, and savings. Its real-time syncing feature ensures that every family member is on the same page, no matter who is making the purchases.

YNAB encourages correcting prioritizing and is especially useful for families who are trying to pay off debt or build their savings. You can set targets for anything you like and track your progress over time.

YNAB also has educational resources and debt management tools integrated within the app making it easy for families to improve their finances.

2. EveryDollar

EveryDollar ( On Google Play / On App Store ) follows a zero-based budgeting system, meaning every dollar of income has a purpose. The app is simple and user-friendly, making it a great choice for busy families who want an easy way to manage their finances without complicated features.

EveryDollar allows families to plan for monthly expenses, track spending, and adjust budgets as needed. The free version offers basic budgeting features, while the paid version, EveryDollar Plus, offers automated bank transactions and other premium features.

Use EveryDollar to ensure every penny is accounted for, making it easier to cover all expenses and save for future goals. Its simplicity is ideal for families new to budgeting.

3. Honeydue

Honeydue is a budgeting app designed for couples but works perfectly for families as well. It allows users to track shared expenses, sync multiple bank accounts, and assign different spending categories. Honeydue shoes members exactly where the money is going and avoid confusion or financial disagreements.

Honeydue also sends reminders for upcoming bills, which is great for families managing multiple payments each month. The app’s chat function encourages communication around money, making it easier for family members to discuss finances openly.

4. Goodbudget

If you’re a fan of the envelope budgeting method, Goodbudget is a fantastic digital tool for families. The app helps families allocate money into virtual “envelopes” for categories like food, rent, and entertainment. It’s a great way to visually manage how much you have left to spend in each category throughout the month.

Goodbudget is perfect for families who want a simple, structured way to stay on top of their finances. It also allows multiple family members to track and manage spending across various envelopes, ensuring accountability and coordination.

Goodbudget provides a structured approach to budgeting and will help families manage their finances. The app can also be used to teach children about budgeting, beginning to build healthy habits early on.

Related: Electric Heaters vs. Central Heating: Which is More Cost-Effective for Your Home?

How Budgeting Apps Help Families

Budgeting apps not only help families stay on top of their expenses but also provide long-term financial benefits. By using these apps, families can:

- Create Financial Transparency: Budgeting apps offer a shared view of household finances, which encourages open discussions and ensures everyone is aware of spending habits.

- Plan for Big Goals: Saving for future goals becomes more manageable, whether it’s setting aside money for a vacation or a child’s education.

- Manage Day-to-Day Finances: Apps provide real-time updates, allowing families to adjust their budgets on the go, whether for groceries, bills, or unexpected expenses.